Dividend Growers

Dividend Growers

Dividend Growers

Dividend Growers

As companies continue to navigate fluctuating pandemic conditions, they are gradually normalizing their capital allocation policies, and stock buybacks are hot again. So, we ask, should dividend growth or a buyback be more appealing to investors? While both stock buybacks and dividends are important components of total shareholder yield, there are important differences to consider.

Recent Dividend vs. Buyback Trends

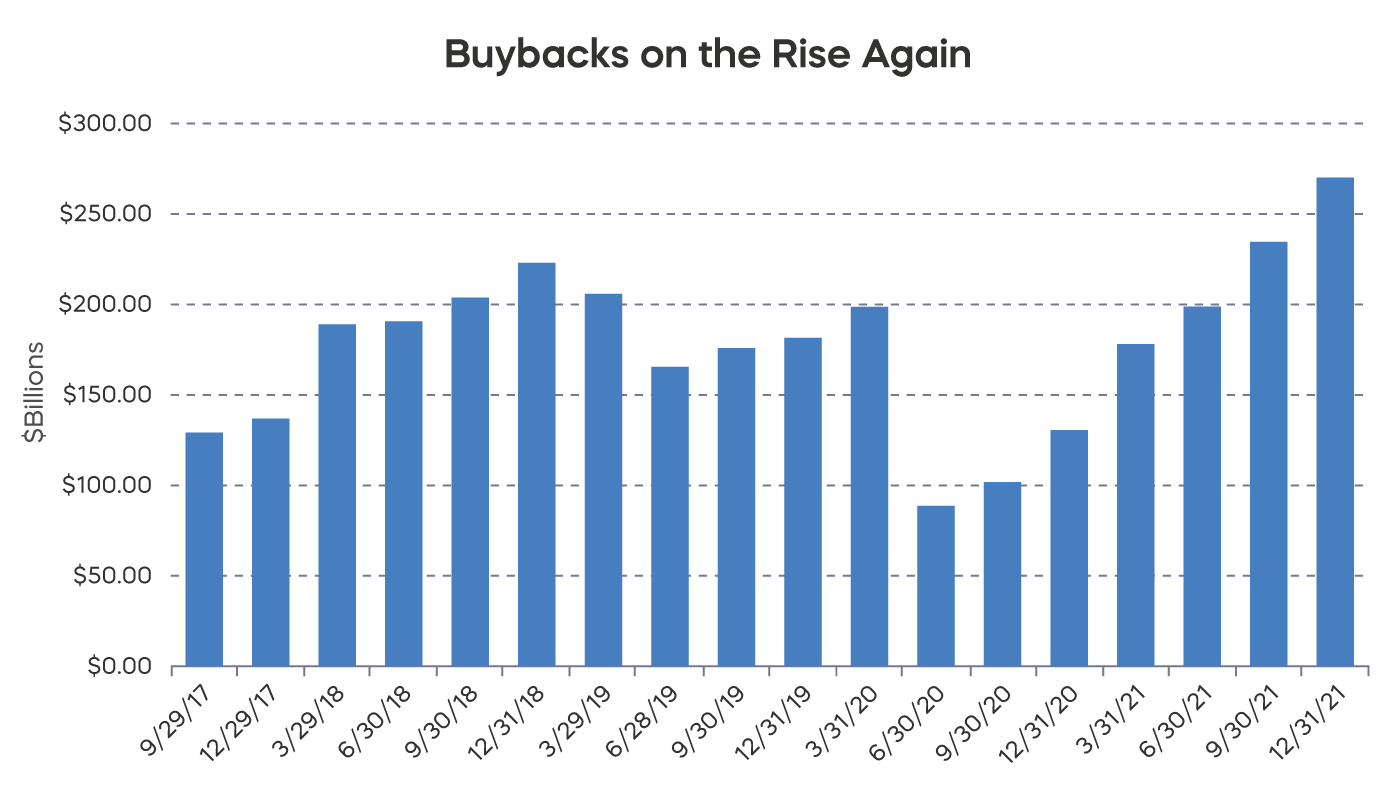

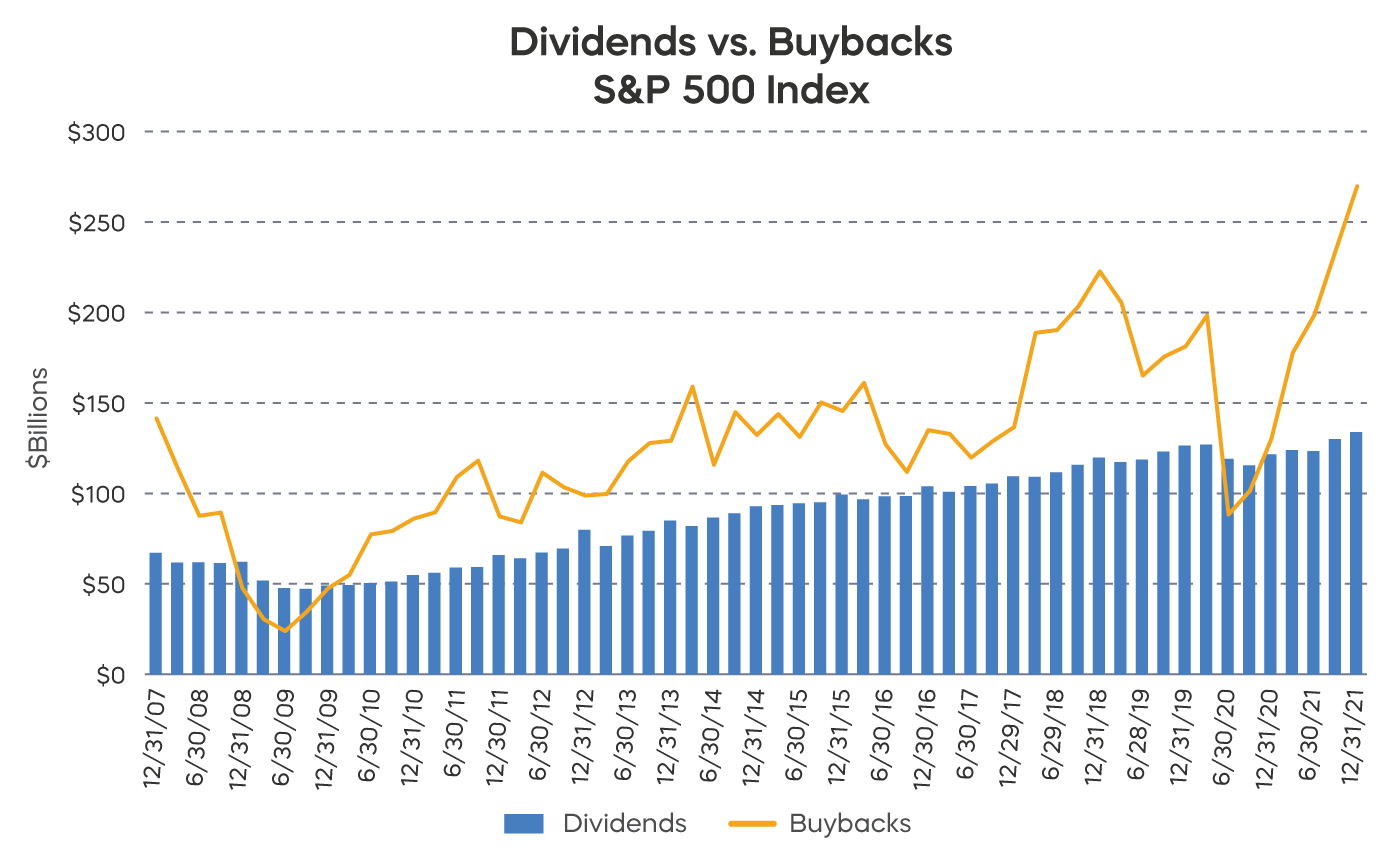

Dividends largely rebounded in 2021, but the volume of stock buybacks has been setting records recently. Standard & Poor’s reported that fourth quarter 2021 buybacks were $270 billion—an all-time high—and up 15% from the third quarter.

Why the Fuss over Buybacks?

- Dividends have long been viewed as a prudent and even expected deployment of capital.

- Buybacks have a more contentious history, and the steady increase in buyback volumes over time has brought scrutiny.

- Increasing EPS, for example, can overshadow a situation where returns on invested capital are decreasing over time on lower incremental returns.

- Leading buyback companies are sometimes the same companies that issue abundant shares in compensation related options.

The Dividend Growth Advantage

-

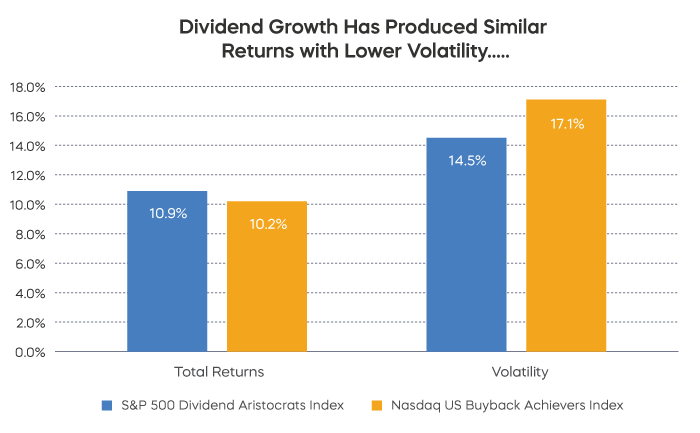

The S&P 500 Dividend Aristocrats are stocks that have grown their dividends for a minimum of 25 consecutive years.

-

The Nasdaq U.S. Buyback Achievers Index tracks companies that have reduced their shares outstanding by at least 5% over the trailing 12-month period.

Comparing Returns over Time

Since common inception, the S&P 500 Dividend Aristocrats Index has generated returns on par with the Nasdaq U.S. Buyback Achievers Index; however, the Dividend Aristocrats Index has produced significantly greater risk-adjusted returns. The buyback index has been significantly more volatile and has exhibited larger drawdowns and down-capture ratios relative to the broad market—an important distinction between the strategies in a market where volatility may linger. Of course, there is no guarantee these indexes will always perform this way.

The Takeaway

As capital allocation policies continue to normalize, investors will be closely watching dividend and buyback activity. While both approaches are investor-friendly components of shareholder yield, there are important distinctions for asset allocators. Dividend growth over time potentially delivers a stronger and more consistent signal to shareholders of a company’s future prospects. In addition, a dividend growth approach has delivered higher risk-adjusted returns over time.

Dividend Growers

Dividend Growers