Leveraged & Inverse

Leveraged & Inverse

Leveraged & Inverse

Leveraged & Inverse

Bond prices and interest rates tend to move in opposite directions. When interest rates rise, existing bonds with fixed coupons typically decline in value. Investors who hold Treasury bonds, Treasury ETFs, or diversified bond funds may want to consider hedging a portion of their interest-rate exposure, particularly if they expect yields to rise or want to try to reduce portfolio volatility without selling their underlying bond holdings.

The rate environment has changed materially since the extended long bond bull market that began in the early 1980s. After reaching historically low levels in the 2010s and early 2020s, Treasury yields rose sharply during the 2022–2023 tightening cycle and remain elevated nowrelative to versus the prior decade.[1] Even after that adjustment, yields can remain vulnerable to upward pressure when inflation proves persistent, energy prices rise, fiscal deficits remain large, or investors demand higher real yields to hold longer-term bonds.

A useful way to think about the 10-year Treasury yield is as the combination of expected inflation and plus a real yield. Over the past several decades, the 10-year Treasury yield has averaged roughly 2%-% to 2.5% above core inflation.[1] But that period includes the post-2008 era of quantitative easing, when longer-term yields were unusually low by historical standards. Before quantitative easing began in 2008, the average real yield on the 10-year Treasury was closer to 3%.[1] If investors demand begin demanding a higher real yield to hold longer-term bonds again, the 10-year Treasury yield could remain elevated or move higher even if inflation moderates. For example, a 3% real yield plus 2% inflation would imply a 10-year Treasury yield near 5%. If inflation remains above the Fed’s 2% target, the implied 10-year Treasury yield could be even higher. This is one reason bond portfolios can remain exposed to rate risk even after yields have already increased meaningfully.

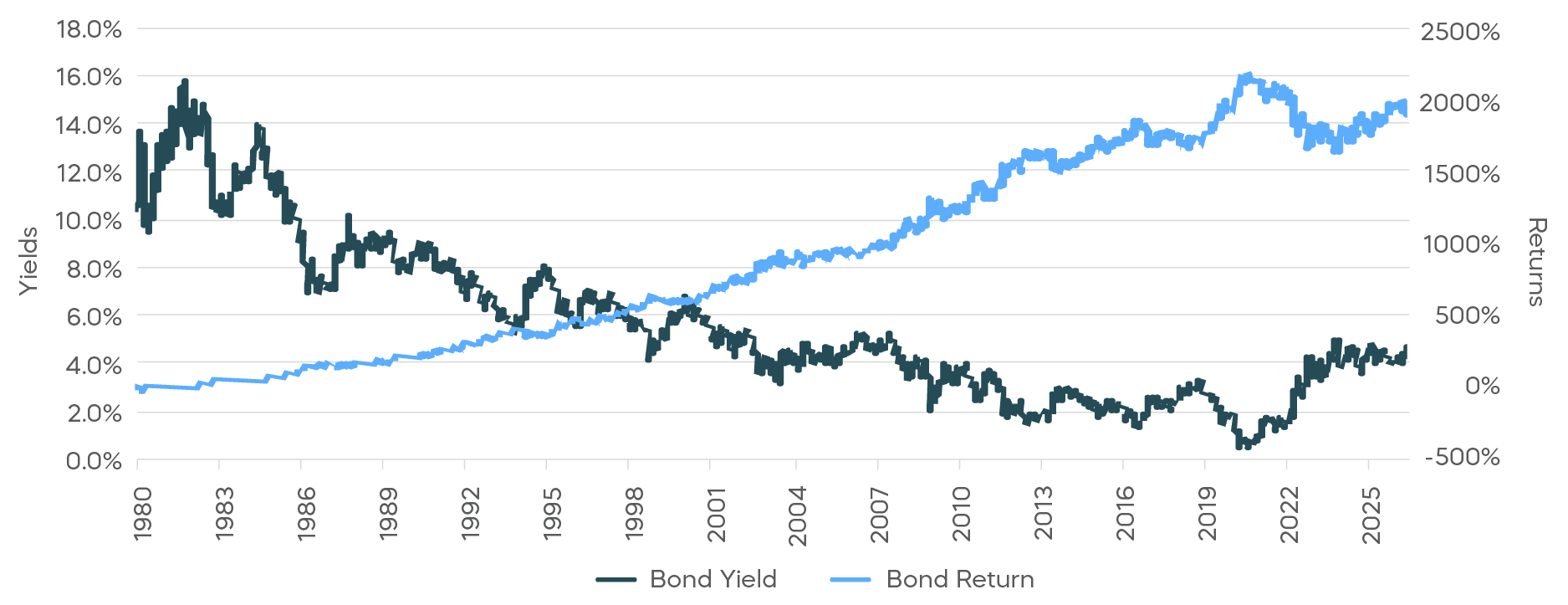

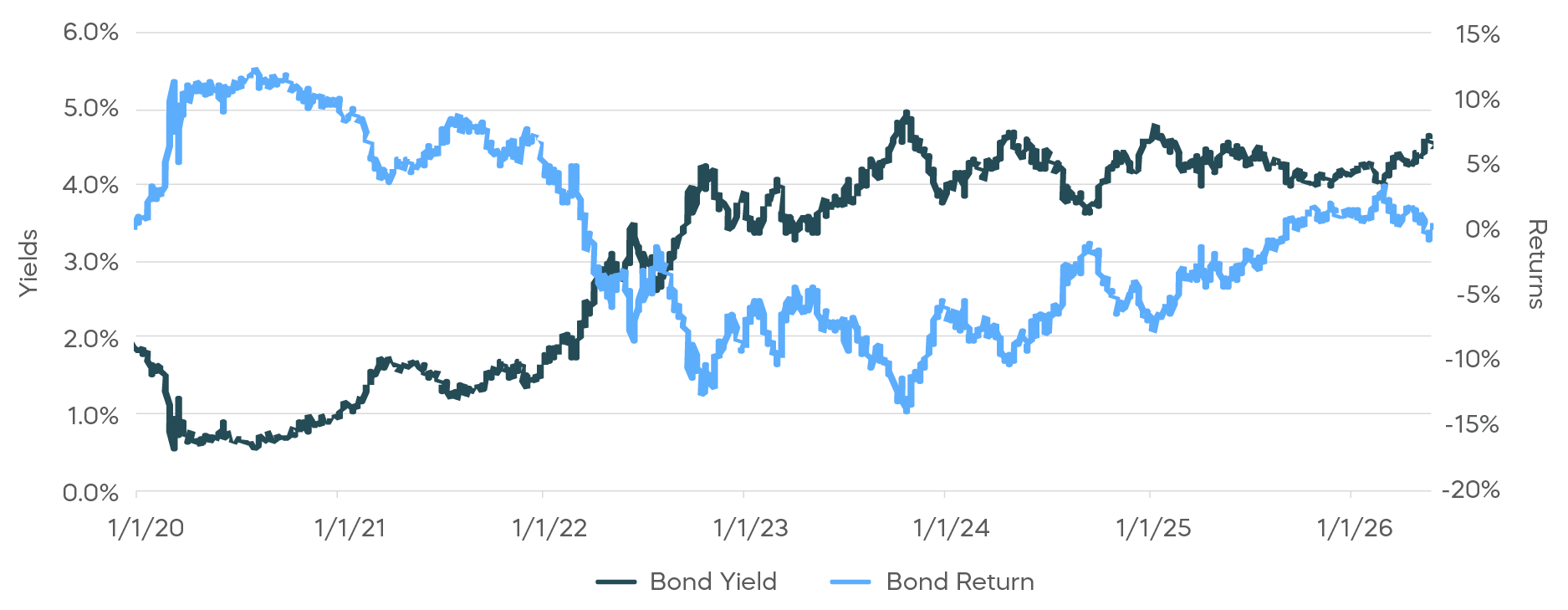

The long-term return profile of Treasury bonds reflects the broader decline in rates from the early 1980s through the 2010s. In total return terms, 7-10 year Treasury bonds have generated a compound annual return of 6.7% since 1980. Since 2020, however, returns have been muted, illustrating how sharply rising yields can offset years of income. The two-panel chart that follows compares the total return of 7-10 year Treasury bonds with the 10-year Treasury yield. The first panel shows the full period since 1980, during which Treasury bonds performed well as yields generally declined. The second panel focuses on the period since 2020 and highlights the effect of the recent rate shock. It includes, including the 2022 selloff and the drawdown through mid-October 2023, when 7-10 year Treasury bonds were down nearly 15% from the beginning of 2020.

Falling yields generally support bond prices, while rising yields can pressure bond prices. The impact depends on duration, maturity, coupon, yield-curve changes, and other portfolio characteristics.

Bond Yields and Returns Since 1980

Bond Yields and Returns Since 2020

Measuring the Impact of Rising Rates

To estimate the potential impact of rising rates on a bond portfolio, investors often look at duration. Duration is an approximate measure of a bond or bond portfolio’s price sensitivity to changes in interest rates. Higher duration generally means greater interest-rate sensitivity. Longer-maturity fixed-rate bonds generally have higher durations, while floating-rate bonds, shorter-maturity bonds and bonds that may be called in the near term generally have lower durations.

As a hypothetical example, long-term U.S. Treasury bonds with maturities of 20 years or more and a duration of 18 should be more than twice as sensitive to rate changes as intermediate-term U.S. Treasury bonds with maturities of 7-10 years and a duration of 8. A 1% rise in long-term Treasury yields could cause the price of the long-term Treasury bond portfolio to decline by approximately 18%, while a similar increase in intermediate-term Treasury yields could cause the intermediate-term Treasury bond portfolio to decline by approximately 8%.

Approximate price change = -Duration x Change in Yield

How Sensitive Is Your Portfolio to Changes in Interest Rates?

Consider a hypothetical $100,000 bond portfolio with a duration of 6. A 1% rise in interest rates could cause the value of the portfolio to decline by approximately 6%, to $94,000. That could potentially offset more than a year’s worth of interest income. A two percentage point increase could drive the value down by approximately 12%, to $88,000. Even a relatively small shift in interest rates can have a meaningful impact on the value of a bond portfolio.

Estimated Impact on a $100,000 Bond Portfolio by Duration

Preparing Your Portfolio for Rising Rates

There are two general approaches to consider in a rising-rate environment: restructuring the portfolio or hedging the exposure.

Restructuring Your Portfolio

Restructuring seeks to mitigate interest-rate risk by changing the portfolio’s underlying positioning. This may include reallocating from longer-duration bonds to shorter-maturity or lower-duration bond investments, moving a portion of the portfolio into asset classes with lower sensitivity to interest rates, or using strategies such as bond laddering. These changes can reduce rate sensitivity, but they may also affect portfolio income, diversification and tax outcomes.

Hedging Your Bond Portfolio

Many investors choose to hedge instead of, or in addition to, restructuring their portfolios. A hedge is intended to move in the opposite direction of the investment being hedged. When bond prices fall, the value of the hedge may rise and partially offset the decline. If bond prices rise, however, the hedge would reduce total returns.

Two common ways to hedge a bond portfolio are short selling a bond investment or buying an inverse bond ETF.

- Short selling a bond investment can provide a hedge against rising rates, but it may require opening and funding a margin, options or futures account. Losses can exceed the initial investment.

- Inverse bond ETFs are designed to move opposite their indexes. They seek investment results that are the inverse, such as -1x or -2x, of the daily performance of a Treasury or other fixed-income benchmark. These ETFs trade on exchanges like stocks, and losses are generally limited to the value of the investment. However, inverse bond ETFs require monitoring, as frequently as daily, and may need periodic rebalancing, which can involve costs and tax consequences. For any holding period longer than a day, returns may be higher or lower than the daily target. These differences could be significant.

What Is an Inverse Treasury bond ETF?

An inverse Treasury bond ETF is designed to move in the opposite direction of a specified Treasury bond benchmark on a daily basis, before fees and expenses. For example, a -1x inverse Treasury ETF generally seeks to rise by about 1% on a day when its benchmark falls by 1%, and fall by about 1% on a day when its benchmark rises by 1%. Because these funds reset daily to target -1x the benchmark’s return for that day, their cumulative return over longer periods can differ from the inverse of the benchmark’s cumulative return. Investors using them for more than a single day generally need to monitor the position and rebalance as needed to maintain the intended hedge size within the broader portfolio.

Hedging with an Inverse Bond ETF

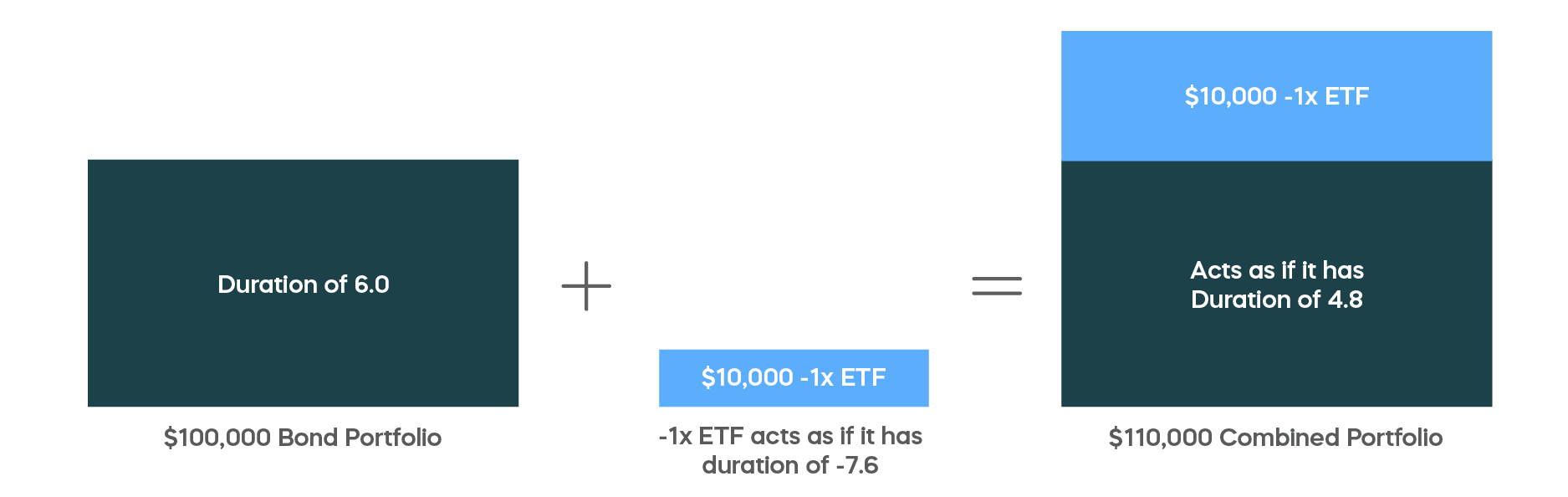

The illustration below starts with a hypothetical $100,000 bond portfolio. An investor who wants to reduce interest-rate sensitivity could add a $10,000 position in an inverse bond ETF as a hedge. In this example, the existing bond portfolio has a duration of 6, while the inverse bond ETF acts as if it has a duration of -7.6. Combined, the $110,000 portfolio behaves as if it has a lower duration of 4.8.

In this example, a 1% rise in rates could cause a hypothetical $100,000 bond portfolio with a duration of 6 to decline by approximately $6,000. At the same time, a $10,000 inverse ETF position with an effective duration of -7.6 could gain approximately $760. The net decline for the combined portfolio would therefore be reduced to approximately $5,240, lowering the portfolio’s effective duration from 6 to 4.8.

How an Inverse ETF Reduces Interest Rate Sensitivity

Matching the Hedge to the Exposure

The straightforward math of duration explains the relationship between changes in yield and price, both for bonds and hedges, when rates move in a broadly parallel way (meaning short-, intermediate- and long-term yields move in the same direction by similar amounts). The match can be less precise when the yield curve steepens, flattens or twists. For example, if short-term interest rates rise but long-term interest rates hold steady, long-term bond prices may not change materially, even though long-term bonds generally have longer duration than short-term bonds. ProShares offers inverse bond ETFs with different maturity ranges to facilitate both the management of duration and the targeting of different parts of the yield curve.

Investors should also consider whether a portfolio includes credit exposure. For example, high-yield bonds are influenced not only by interest rates, but also by changes in credit spreads and the health of corporate borrowers. In those cases, a Treasury-focused inverse ETF may not fully address the portfolio’s risk, and investors may need to consider whether a high-yield or broader fixed-income hedge is more appropriate.

Advantages of Using Inverse Bond ETFs

Using inverse bond ETFs to hedge interest-rate risk can complement longer-term portfolio strategies. They can help investors reduce rate sensitivity without selling existing bond holdings or making permanent changes to a strategic allocation.

Inverse bond ETFs can help investors:

- Keep asset allocation in line with long-term investment goals by adding or removing hedge exposure as needed.

- Hedge existing bond positions instead of selling them, which may help avoid disrupting income plans or realizing taxable gains.

- Use a smaller capital commitment than may be required to restructure a larger bond portfolio.

- Avoid some of the operational complications of short selling, such as opening a margin account or maintaining required account balances.

- Limit losses to the value of the ETF investment, unlike a traditional short position where losses can exceed the initial investment.

Considerations for Using Inverse ETFs

Most inverse ETFs aim to provide a multiple of the return of a benchmark for a single day, before fees and expenses. To maintain their investment objectives, inverse ETFs rebalance their exposure to their underlying benchmarks each day. As a result of daily fund rebalancing, an investor holding an inverse ETF longer term is unlikely to continue to receive the fund’s multiple of its benchmark’s returns. Over time, compounding can cause the investor’s exposure to the underlying benchmark to deviate from the ETF’s stated objective. Investors using inverse ETFs over periods longer than one day are encouraged to actively monitor their investments, as frequently as daily, and to consider a rebalancing strategy for their holdings.

Inverse investing is not for everyone. Inverse ETFs are generally riskier than ETFs without inverse exposure. Before investing, read each fund’s prospectus to fully understand all the risks and benefits. For a prospectus and other information, visit ProShares.com.

1. Source: Federal Reserve Bank of St. Louis. Market Yield on U.S. Treasury Securities at 10-Year Contant Maturity as of 5/28/26.

Learn More

TBF

Short 20+ Year Treasury

TBF seeks daily investment results, before fees and expenses, that correspond to two times the inverse (-1x) of the daily performance of the S&P ICE U.S. Treasury 20+ Year Bond Index.

TBX

Short 7-10 Year Treasury

TBX seeks daily investment results, before fees and expenses, that correspond to the inverse (-1x) of the daily performance of the ICE U.S. Treasury 7-10 Year Bond Index.

SJB

Short High Yield

SJB seeks daily investment results, before fees and expenses, that correspond to the inverse (-1x) of the daily performance of the Markit iBoxx® $ Liquid High Yield Index.

TBT

UltraShort 20+ Year Treasury

TBT seeks daily investment results, before fees and expenses, that correspond to two times the inverse (-2x) of the daily performance of the ICE U.S. Treasury 20+ Year Bond Index.

PST

UltraShort 7-10 Year Treasury

PST seeks daily investment results, before fees and expenses, that correspond to two times the inverse (-2x) of the daily performance of the ICE U.S. Treasury 7-10 Year Bond Index.

TTT

UltraPro Short 20+ Year Treasury

TTT seeks daily investment results, before fees and expenses, that correspond to three times the inverse (-3x) of the daily performance of the ICE U.S. Treasury 20+ Year Bond Index.

Leveraged & Inverse

Leveraged & Inverse