With each passing day, investor focus is widening from the near-term impact of spiking oil prices to how—and where—higher energy costs will filter through the broader market.

Energy Drivers: Strait Closure vs. Infrastructure Risk

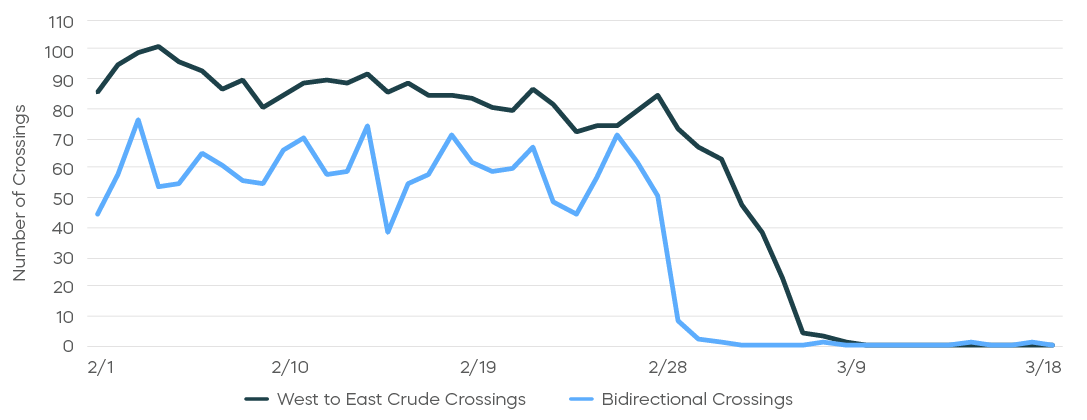

Weekend comments from President Trump extended a Monday deadline to reopen the Strait of Hormuz, prompting crude prices to dip and stocks to rally. However, the Strait remains effectively closed, with Iranian officials signaling no public plans to comply.

For markets, the more lasting development may be the recent escalation of attacks and threats targeting energy infrastructure.[1] Israel’s strike on the South Pars gas field (Iran/Qatar) on March 18 and Iran’s attacks on Qatar’s Ras Laffan liquefied natural gas (LNG) facility on March 18 and 19 highlight growing risks to assets that are central to global natural gas and LNG supply.[2] QatarEnergy estimates that the Ras Laffan attacks have already reduced capacity by about 17%, with recovery potentially taking years,[3] conditions which point to a more structural supply disruption rather than a temporary shock.

Strait of Hormuz Tanker Crossings Have Essentially Stopped

Source: Bloomberg, as of 3/19/2026

Supply Impact: Structural Damage Emerging

Widespread and persistent disruption of such operations may impact prices even more than the Strait closure alone. While the shutdown is currently blocking an estimated 126 million barrels of crude per week, infrastructure damage appears to be reducing regional LNG supply by more than 2.5 billion cubic meters (bcm) per week, based on our estimates derived from long-term IEA supply data.[4]

If attacks continue, the impact could constrain production and export capacity over a multi-year horizon—potentially supporting a long-term increase in global energy prices.[5]

Where the Impact Spreads Next

After several weeks of disruption, analysts are increasingly focused on where sustained higher input costs (and potential cost increases on end consumers) may pressure margins or dampen demand across industries. For example, Bank of America notes that rising energy and fertilizer costs are already putting pressure on a range of agricultural commodities.[6] Markets most exposed to energy cost pass-through, primarily Europe and Asia, may be particularly vulnerable in the next phase of this shock.[7]

1. Source: Bloomberg, data as of 3/20/2026

2. Source: Bloomberg, data as of 3/19/2026

3. Source: Reuters, as of 3/19/2026

4. Source: International Energy Agency and ProShares calculations

5. Source: Bloomberg, as of 3/19/2026

6. Source: Bank of America, as of 3/17/2026

7. The Wall Street Journal, data as of 3/23/2026